Your cart is currently empty!

Employer Health Plans vs. Medicare: Should You Switch?

As more Americans work beyond age 65, many find themselves wondering whether they should stick with the health insurance they receive from their employer, or switch to Medicare. On the surface, staying with your current health plan might seem like the easiest option; you know your doctors take it and know what costs to expect. But depending on your situation, staying with your “work plan” could end up costing you more.

Here’s what you need to know to make an informed decision.

The Basics: What Happens at Age 65?

At age 65 you’re eligible for Medicare, the federal health insurance program that covers hospital care, medical services, and prescriptions. But if you’re still working and receive employee healthcare benefits, Medicare eligibility doesn’t mean you have to leave your employer plan. However, doing so might save you money or allow you to receive better benefits. Whether you should keep or leave the employer sponsored plan depends on your job situation, the size of your employer, and your financial and medical needs.

Let’s take each of these point by point:

Your Job Situation: Are You Still Working Full-Time?

If you’re still working and actively covered under your employer’s group health plan, you might not need to make any changes right away. In fact, many people continue on their employer plan without enrolling in all parts of Medicare if they like their coverage or are contributing to a Health Savings Account (HSA).

On the other hand, if you’re working part-time or your employer is offering limited coverage, then switching to Medicare might provide less expensive or more complete benefits. This is especially true if you’re paying a large portion of the premium yourself. If you’ve officially retired but your employer is still offering COBRA or retiree coverage, keep in mind that those options do not count as “active employer coverage” for Medicare purposes. This means that if you don’t have active employer coverage, delaying Medicare enrollment could result in penalties.

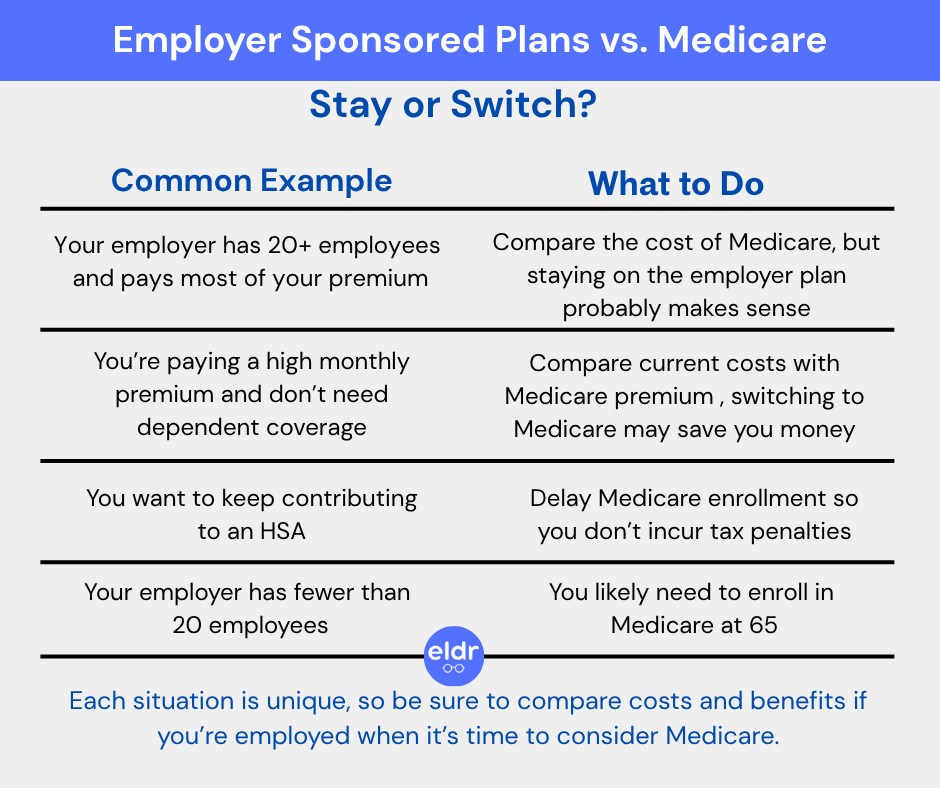

The Size of Your Employer: Why 20 Is The Magic Number

This is one of the most important factors in your decision. If your company has 20 or more employees, your employer coverage is considered primary insurance, and Medicare is the secondary insurance. That means you can delay enrolling in Medicare Part B (and Part D) without penalty. You’ll qualify for a Special Enrollment Period (SEP) when you retire or lose your group coverage, allowing you to sign up for Medicare at that time without late fees or coverage gaps.

But if your company has fewer than 20 employees, the rules flip and Medicare becomes your primary insurance, and the employer’s plan pays second, if at all. If you delay Medicare enrollment in this case, you might not be covered for services Medicare would normally pay for, and you could end up footing the bill yourself. In short: if your employer is small, don’t wait to sign up for Medicare at 65.

Your Financial and Medical Needs: Compare Costs and Coverage

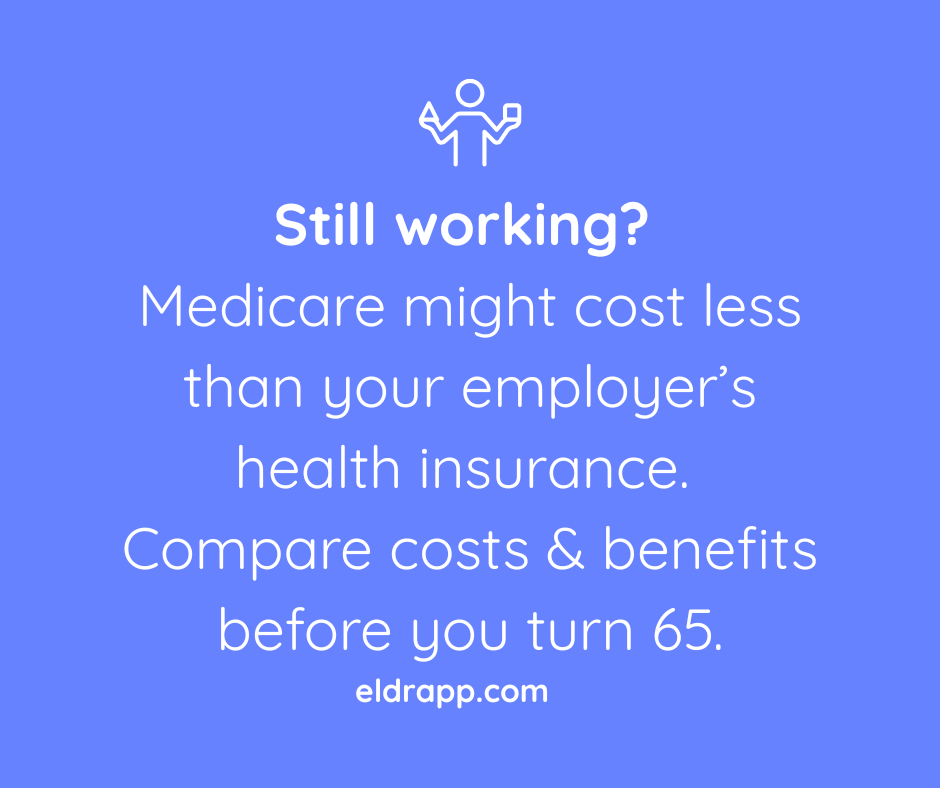

Even if you’re happy with your employer plan, it’s worth comparing the total costs of staying on that plan versus switching to Medicare. Start by looking at your monthly premiums, co-pays, deductibles, and drug costs. Many people are surprised to find that Medicare is actually more affordable, especially when you add a Medigap or Medicare Advantage plan to help with out-of-pocket expenses.

For example: in 2024, most people paid $174.70/month for Medicare Part B. Some Medicare Advantage plans have $0 premiums and include extra benefits like dental, vision, hearing aids, and even fitness programs. If you’re paying $400 or $500 a month for your job-based plan, Medicare could offer similar or better coverage at a lower cost.

Also consider your medical needs. If you have a chronic condition, need frequent care, or require prescription drugs, check whether your employer plan or a Medicare plan offers better access to the services you rely on. Medicare Part D or Advantage plans may offer stronger drug coverage, while some employer plans limit access to specialists or out-of-network providers.

On that note, while almost all doctors take Medicare, not all doctors will take your specific plan. A doctor might accept Medicare, meaning they take Original Medicare from the federal government, but that doesn’t automatically mean they accept every Medicare Advantage plan (like those from United, Humana or Blue Cross for example). Yes it’s confusing, so if you’re considering Medicare and don’t want to switch doctors, be sure to sign up for a plan that your doctor takes.

A Word About HSA’s

Once you enroll in any part of Medicare you’re no longer allowed to contribute to a Health Savings Account (HSA), because the IRS only permits HSA contributions if you have a high-deductible health plan with no other coverage. Since Medicare counts as additional health coverage, continuing to contribute would violate IRS rules and could result in tax penalties. Many people delay Medicare enrollment specifically to keep contributing to their HSA while still working.

As you approach 65, compare your health insurance options. Speak to your HR department, review your health plan’s costs and coverage, and consider talking with a Medicare advisor. A little homework now can save you thousands later and ensure you’re getting the coverage that’s right for your needs.

Leave a Reply